Post Menu and Details.

Words: 1021

Reading time: ~4 minutes

Do you know the reasons why people take personal loans? Personal loans are very popular, especially last year when health and financial issues impacted people’s lives all over the world. But what are the most common reasons to take a loan?

Actually, there are several common causes typical for most people. You can ask, — When going for personal loans does it matter the reason why I need the loan? The answer is yes; the reason does matter because, in many cases, it determines the rates, terms, and conditions of the loan. But let’s discuss every reason and see the differences.

Personal Loans: Do I Have to Give the Reason?

In short: yes, you have to. Approval of your loan depends on the reason you named. Sometimes the reason can also affect the rates and terms of the loan. So you need to think through considering personal loans what is best to select for the reason of use. It will save you time and money.

Popular Ways to Borrow Money

Now we know the reasons people take loans. Let’s talk about the most common sources.

1. Banks. The most traditional way of borrowing money is to go to the bank. Modern banks offer a wide range of personal loans and other financial products.

2. Lending services. They are financial organizations specializing in different forms of loans. They often offer attractive terms, and their popularity is growing.

3. Credit cards. Credit cards suit best for small regular purchases. They usually have strict limits and offer a small amount of money, but the terms can be very good. They can offer a grace period, and it’s really beneficial for small purchases. On the flip side, credit cards can carry exorbitant interest rate charges if a balance is carried over.

4. Different apps. Money-borrowing apps have become more and more popular because of convenience. You can get money by making several clicks. The terms can differ a lot, so you have to choose carefully.

#1 Financial Problems

This year we witnessed a downfall in almost all economic sectors. It resulted in reduced incomes of salaries. The payment of self-employed individuals also came down. In order to deal with gaps in income, many people opted for personal loans. It’s also the reason for the high interest rates for personal loans to decrease in the past few months.

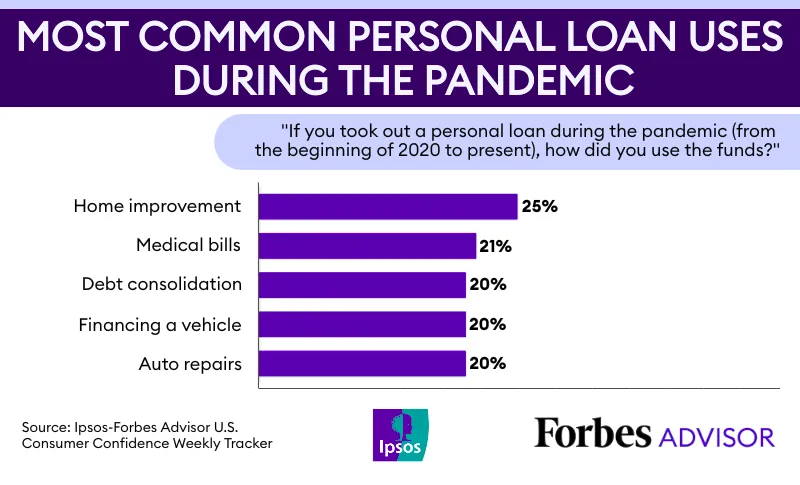

#2 Payments for Medical Care

Medical bills are the second most popular reason why people took loans last year.

Unfortunately, health problems are still one of the most common reasons for personal loans. Facing the need for an operation or an expensive treatment, people usually have no choice other than to go to a bank or financial organization. In most cases, personal loans are the easiest way to pay for medical bills.

#3 Other Credits

It may look strange, but people often take loans to repay the other debts. It can be done to pay several loans and only have one left, in other words, for debt consolidation. It helps to save time and sometimes money because of the various rates for personal loans depending on the reason. This year many banks offered special Covid schemes which help people with debt consolidation.

#4 Insurance Payments

All types of insurance are to be paid every year. Many households prefer taking a loan for the annual payments and keeping all the benefits. Actually, it’s a consequence of the first reason, in other words, people have troubles with income and have to take out a loan in order to keep their lifestyle.

#5 Money for Investments

The global economic crisis has become a disaster for many people, but for investors, it’s also an opportunity to buy assets for future gains. This year investments are the common reason for loans. Although lending services usually don’t approve loans for investing in stocks, borrowers can choose from the best personal loans for any reason they can think of.

#6 Mortgage Payments

Even in hard times, it’s not wise to miss mortgage payments. People are afraid to lose their homes, so they rely on personal loans in case of reduced income. It’s not a bad decision because missed payments can accumulate additional interest or cause penalties. A personal loan can be a temporary solution allowing one to buy some time and find an income source.

#7 Money for Purchases

Life goes on and loans for purchases are the most common. People need money to buy laptops, smartphones, personal computers, etc. to work from home and make money. Different kitchen equipment, TVs, washing machines, etc. are also popular among customers. People prefer convenience and personal loans allow them to buy a necessary thing in no time.

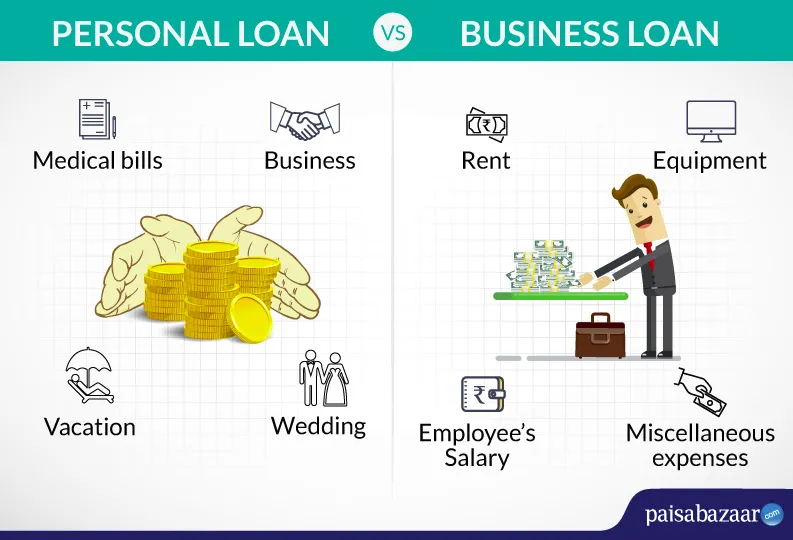

#8 Money for Business

Of course, there are special business loans, but they aren’t always convenient. Besides, it can be hard to receive money if your company has a bad credit score or doesn’t have any. In such cases, many people apply for personal loans.

These loans are fast, and you can receive money in several days and considering a large number of apps that let you borrow money, it takes only a few clicks. Of course, this option is suitable only if you need a small amount of money.

But you should clearly separate business loans and personal ones.

#9 Money for Personal Vehicle

People like the comfort of their own car, and in a pandemic situation, it’s also a safety issue. You can apply for a car loan to buy a new vehicle, but personal loans are very popular for the second-hand market.

This trend is also common for two-wheelers. Considering rather low prices for bikes and used cars, choosing a personal loan is usually a good idea because of slightly lower rates.

#10 Money for Down Payments

Like in the case of investments, people can use the economic situation to make a bargain and buy a house for a lower price. Usually, personal loans are used only to make a down payment. The same holds for other big purchases and kinds of property. This trend shows us that even a bad economic situation can give some opportunities for good investments.

In conclusion, no matter what reason you have and what way of borrowing you prefer, always make sure that you carefully analyze all available options and study all the terms.

Thank you for reading!